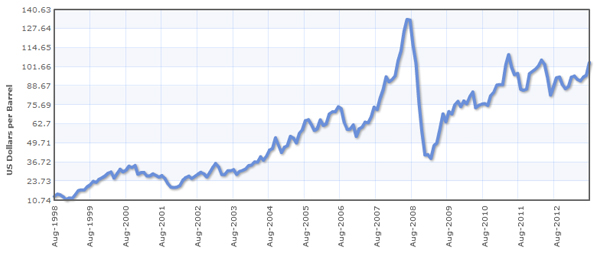

Because of the focus on the financial collapse and the bailing out of banks, it’s easy to forget the role of oil in the recent economic turmoil. The great big spike in 2008, and the collapse immediately afterwards, has complicated the trend. Five years on, it’s easier to see through the disruption and identify the long term trends in the long term price of oil. Here are the last 15 years:

The 1970s was a messy decade for the oil price, with a series of crises and corresponding economic chaos. By the mid-80s the price had settled again at a steady low, allowing for 15 years of uninterrupted oil use and an understandable complacency about oil dependence. That began to change around the turn of the century, and from around 2003 the current trend begins: the inexorable rise of the price of oil.

There are a host of reasons why. The most obvious is booming demand. As countries develop, more and more people take up a long-promised Western lifestyle, complete with driving and flying. At the same time, conventional oil production began to plateau. As predicted, there was a rush towards unconventional fuels and renewed investment in gas. Oil companies began to look further afield for new sources of oil, offshore or in the Arctic circle. Events in the Iraq, Libya, and elsewhere in the Middle East continue to disrupt supply, with speculators exaggerating the effect of each perceived threat.

The pumps are still flowing, but it’s not cheap any more. It can’t be – shale or deepwater oil is more expensive to extract. It wouldn’t be economic at the $40 a barrel prices we used to know. At this point, the normal rules of supply and demand ought to kick in. First, a rising price ought to signal demand, which in turn should increase supply. That’s proved harder than expected, as there’s very little spare capacity in the system. Increasing supply takes time and investment, and it’s been slow to come online. Quite how much higher production can go is anyone’s guess.

Second, you’d expect there to be a degree of demand destruction, as the high price deters people from driving. That’s happening in developed countries, but globally demand continues to rise. That’s partly because some developing countries are subsidising oil use and cushioning citizens from rising prices, and partly because there are no straight swaps for oil. There are no obvious alternatives, or certainly nothing that can be brought online quickly.

The upshot of all of this is that the oil price continues to cast a shadow over the economy. There are optimistic stories every other day offering new evidence of economic recovery and a return to growth (though those are not the same thing, IMO), but that recovery is vulnerable to the movements of the oil price. Brent Crude is around $116 a barrel as I write. Should the US move on Syria, that’s likely to jump above $120. If it spikes, well, we know what that tends to do.

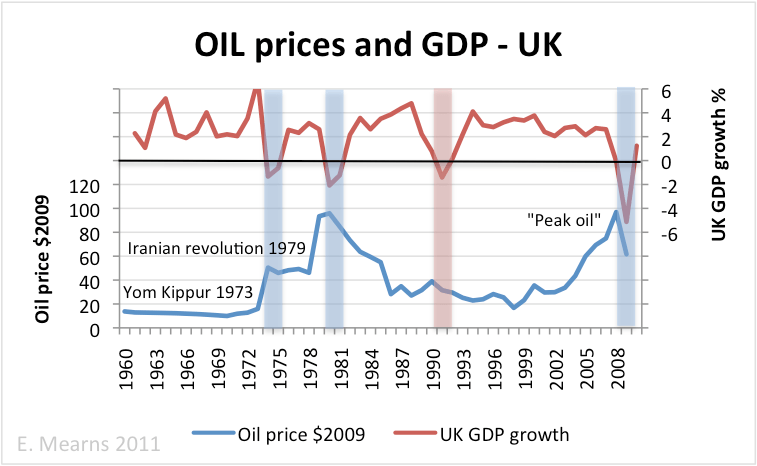

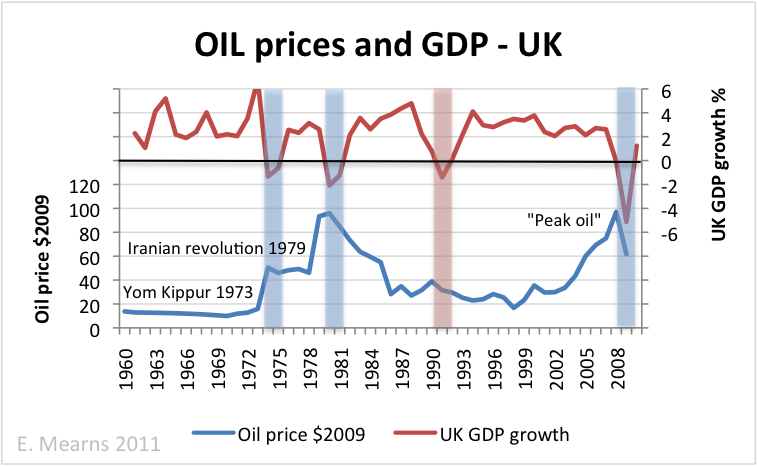

The graph above shows UK recessions in response to the oil price (the blue ones). It’s not a straight-forward relationship, but many commentators believe we’ve entered a new era in the economics of energy. Jeff Rubin, writing during the recession, predicted that “the moment the economy stops sputtering and comes back to life, oil prices will resume their upward trend.” But then, “the price of crude will keep going up until it triggers another downturn.”

Nafeez Ahmed sees “an undulating production plateau correlating with higher but more volatile oil prices, as well as a prolonged recession punctuated by small cycles of ‘recovery’ and contraction.” Richard Heinberg goes further and says that “we have in fact reached the end of the era of fossil-fueled economic expansion.”

There may be positive signs from some sectors of the economy. But until we deal with our oil dependency, it remains a fragile thing.

The days of cheap energy are over. The oil price has fallen back a bit over the last few days as war in the middle east seems less likely, but it still very high.

http://www.theoillamp.co.uk/?p=2871

The oil price is going to be volatile for a while, as thing go back and forth over Syria. We might be lucky and escape a spike over Syria, but it’s hardly going to be the last threat to oil supplies.

What I find bizarre is the complete absence of the role of oil in political debate. It’s somehow invisible as a risk or as a factor in the health of the economy.

Good article and agree with perception-economic recovery will depend on the price of oil no other relevant answer makes sense-so buyer beware.

great points altogether, you just received a logbo new reader.

What would you recommend in regards too your put up

that yoou simply made a ffew days ago? Any positive?