Remember George W Bush landing on the aircraft carrier with a big ‘mission accomplished’ banner hanging in the background? The coalition government is currently going through a similar moment, taking every opportunity to congratulate themselves on Britain’s economic recovery. (You can do your own Google image search for the Photoshop hack of Cameron on the flight deck of the USS Abraham Lincoln)

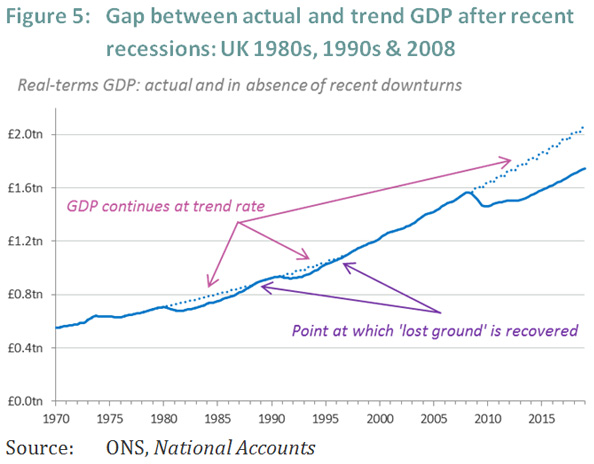

It’s true that fewer people are out of work, that the housing market is moving, and that GDP is up. But the economy hasn’t made up the ground it has lost, and doesn’t look likely to any time soon. Wages have stagnated while prices have risen, so most of us are poorer today in real terms. And the recovery is not driven by investment or exports, but by consumer spending and new debt.

This is all detailed in a rather striking post-budget briefing note from the Resolution Foundation, a think tank focused on low and middle income households. “The strength of the economy in 2013 was primarily based on consumer spending” they warn. “Yet household incomes have not kept pace with this spending, meaning that the recovery has instead been built on a willingness among households to draw down savings and take on new unsecured borrowing.”

Debt was responsible for much of Britain’s pre-crash growth. People withdrew equity from their houses or took on unsecured debt on credit cards and easy personal loans. That slowed dramatically during the crisis, and is now picking up again, but we start from a much higher level of indebtedness.

We now face an unenviable choice, suggests Matthew Whittaker, senior economist at the Resolution Foundation: “Re-stoke private debt and risk generating the same problems of instability encountered during the last boom, or wean the economy off its credit addiction but face permanently lower levels of real growth.”

The first option is inherently unsustainable, and will end with another debt crisis at some point. The second option essentially puts the British economy onto a GDP slow lane, where growth never returns to the pre-crisis trend line. We’d be in a new normal of slower growth.

The Resolution Foundation paper doesn’t come from a postgrowth perspective, but it is a whisker away from what I’ve been suggesting about Britain already being a post-growth economy and just not knowing it yet. Or what Richard Heinberg says in his book The End of Growth. Or Tim Morgan of Tullett Prebon, who forecasts a permanent slump in which “the UK economy is likely to do little better than mark time”. James Rickards explains how our problems are structural rather than cyclical in his new book The Death of Money, and thinks that we are in a depression.

They’re all coming from different perspectives, but with one common theme: return to business as usual is unlikely. There are a whole cluster of factors – debt, demographic transition, higher energy prices – that are combining to create a new low-growth reality.

As I’ve written about before, that should not be considered the end of the world. I suspect it is inevitable, the natural end point of a mature industrial economy. But that doesn’t mean we can relax. Growth can’t just be turned off, and the urgent thing now is to plan for a low growth environment. The worst thing we can do is what we’re currently doing – tapping private consumption for the illusion of growth, as that will simply pile up into a debt crisis when the growth to pay it off fails to materialise. That is quick-fix growth to get us past the next general election.

I might be wrong. I am well aware that mine is a minority view, and I’d be happy to hear about it if anyone does see a way out of the rabbit hole we appear to have gone down.

What do you get when you have a mature capitalist economy, looming resource constraints and a declining global environment?

http://www.abc.net.au/environment/articles/2014/03/25/3970411.htm

I think treading water will be considered doing well in the future and more likely down the slippery slope of living standards.

There are a number of factors involved. People collectively cannot afford to buy the things the produce without getting into debt. This leads to the phenomenon of apparent overproduction. Marx called it “overproduction” and Keynes identified it as “missing demand”. Neither explanation is plausible if examined – there is something else going on here.

As regards GDP, this is a nonsensical measure of the economy. Presumably clearing up after the winter floods will bulk up the figure this year, just as clearing up after an oil spill will. But for what it is worth, it has been estimated that the tax system has a deadweight loss of between 12% and 30% of GDP – that is production that does not take place due to the disincentives built into the tax system.

I don’t think the the Coalition have said the lost ground has been recovered. That is why they are cutting for another 5 years.

Of course GDP misses out on a lot of gains we make. It very much under values the consumer surplus created by new innovative products. The internet, Google and Wikipedia has put vast swaths of human knowledge at our finger tips, connecting us in was impossible to imagine. It has been a huge boon for humanity yet GDP only measures the turnover it creates minus the less efficient businesses it closes. A few months ago someone looked at a 1991 American electrical retailers advert and saw that not only was almost everything now available within the iPhone, but 1991 those things separately would have cost $3000 ($5000 in 2014 money) and an iPhone is $500 today. A lot of that benefit would not be captured in GDP. Certainly the economy is not 10 times bigger.

http://www.techpolicydaily.com/communications/much-iphone-cost-1991/

That isn’t all, of course. The iPhone is much better than just those things. To buy what an iPhone can do in 1991 would have cost over $3.5 million. That certainly isn’t captured in GDP. A it doesn’t even stop there. The money isn’t the important part. The important part is the shear amazing utility of having this supercomputer in your pocket. The benefits are almost impossible to but a cash value on but we can tell how valued they are by the amount of time people spend using them and how bereft they feel without them. That is consumer surplus. GDP doesn’t capture that but it has improved our living standards even in a ‘declining’ economy.

Indeed, and there are other ways in which living standards can improve while GDP does not, as Japan has proved. The problem comes when GDP becomes a policy goal, as it can lead to policies that actively pursue nominal growth while underlying real growth is absent or in decline.

To be fair to the coalition, there is a difference between the official pronouncements of senior figures, and the off-the-cuff comments of backbenchers. Osborne has certainly been quite clear that there is a lot left to do, but that’s not the message coming from the party generally, who want to make it clear ahead of the election that the economy is ‘back on track’.

The economy is not on track, taking the country as a whole. If you don’t believe me spend a couple of days in Newcastle and count the estate agents’ boards.

There is a very good political reason why the Tories want the message to be, “there is a lot to do but our plan is working.” For the last 40 years it seems if the economy is going well then the voters will put in Labour to spend, if it is going badly they back the Tories to fix it. So the Tories always want an economy that is in fragile recovery, Good but unable to withstand Labour running it.

Both parties are useless. The boom-bubble-bust cycle runs on regardless of who is in power. The Tory notion of “recovery” is to generate an asset bubble but it would have happened without their help. Labour’s thought that what was just a bubble was sustainable growth, until the bust came. They are all wasters, but Labour are the bigger wasters. This will continue until a more accurate and realistic model of the economy is adopted by the academics, which is not going to happen any time soon.

The UK electoral system makes matters worse as it allows no room for other views to move in. Effectively, the “opposed” parties are colluding to set the terms of public discussion. It is little more than a game, and no wonder so many people do not bother to vote. Meanwhile the country slowly decays, except in the bottom right hand corner.

It wasn’t the original plan of course. The tories have switched strategy unannounced. It was supposed to be a manufacturing led recovery, the ‘march of the makers’ as Osborne put it. That hasn’t materialised and with the election on the horizon, they’ve decided to take the asset bubble route instead

.

Osborne is part time chancellor, part time Conservative party strategist after all.

Britain cannot manufacture. Labour costs are too high, for a start. For every £1 in real purchasing power of wages, the employer incurs a gross labour cost of about £1.80. That is slow death for the economy.