Last week I read Richard Davies’ book Extreme Economies, and one of the places he investigates is Japan. In the course of discussing an aging population, he mentions some theories around life-cycle economics. In the 1950s, Italian economist Franco Modigliano suggested that people live their economic lives in three acts, moving from dependency to maturity to retirement.

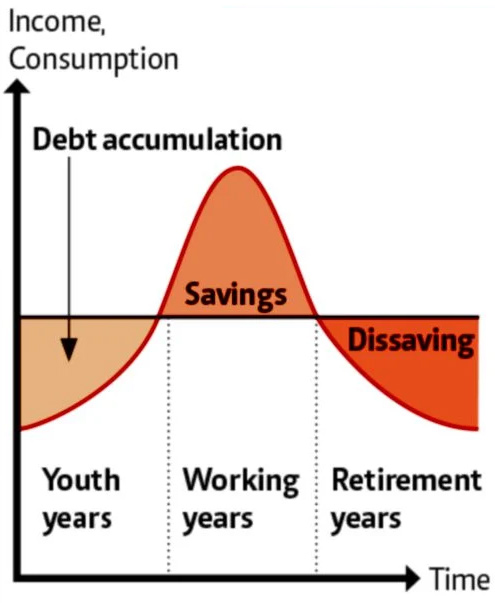

Putting aside childhood and youth, which are obviously the first stages of dependency, the first part of our economic lives are marked by debt. We take on debt to pay for education or to buy a home.

As we get older, Modigliani argued, income increases and we begin to pay down those debts. We salt away some savings, and start to build a stock of wealth.

This stock of wealth is then used in retirement, once we no longer draw a salary.

This is obviously a simplified model that doesn’t apply to everyone. But generally speaking, wealth tends to form a bump throughout our lives, building up and being drawn down.

Understanding this at the individual level can help to plan for retirement and think ahead. At a national level, it helps to plan pension spending, especially when a population is aging and there is less saving going on.

What it made me think of though is national economies. In early stages of development, countries might need to borrow to invest. Then infrastructure is laid down, cities are built, institutions are created and a stock of wealth and resources accumulates. A form of maturity emerges.

This isn’t theoretical. It can be seen in things like steel demand, which tapers off as countries reach a certain point of development. There is a levelling off point when people have enough energy, roads, railways and homes. Construction doesn’t cease, but there’s a visible difference between a rapid development phase, and the maintenance and replacement phase that comes later. This can be tracked in national material footprints data.

Does a third stage of development follow maturity? When population begins to decline, infrastructure ages and institutions struggle to keep up? History suggests all civilisations rise and decline. It also suggests that plenty of civilisations thought that decline was not inevitable and they would be the exception.

What I find interesting is that while history and lived experience suggests stages of development, economics only recognises one of them: growth. Expansion is normally something that characterises the early stages of something. Growth leads to maturity. Not in economics. Here, growth goes on forever. Decline, or even pause, is unthinkable. Any stutter in GDP growth is a cause for alarm.

Unfortunately, with little mainstream economic thinking around maturity and decline, governments orient their policies around growth and growth alone. When it fails, you throw more money at restarting it, at the risk of driving inequality or environmental damage. But if these stages are more or less inevitable, then we miss the opportunity to live well in times of maturity, and fail to plan for decline. It makes those stages fraught and divisive, in ways that they don’t need to be. Economies should be able to age gracefully, stewarding their wealth to ensure that it translates into good lives.

Individual life cycles are not the same thing as national histories, and individual earnings and savings are not the same as national economies. But there are parallels that are easily observable, and if you want to think more about the economics of maturity, it is the subject of my book with Katherine Trebeck, The Economics of Arrival: Ideas for a Grown-Up Economy.

{kind=link}